Federal Direct Loans

Federal Direct Loans, from the William D. Ford Federal Direct Loan (Direct Loan) Program, are low-interest loans for eligible students to help cover the cost of education at Pratt Institute. Eligible students borrow the funds directly from the U.S. Department of Education through Pratt.

Direct Subsidized Loans — are for students with financial need. Pratt reviews the results of each Free Application for Federal Student Aid (FAFSA) and determines the amount each can borrow per year. Students are not charged interest while in school at least half-time and during grace periods and deferment periods (this does not apply to forbearances). If a student graduates, leaves school, or drop below half-time enrollment, there will be a six-month grace period before repayment begins. Undergraduate students are allowed to borrow Subsidized Loans Annually up to the following limits: Freshman – $3,500, Sophomore – $4,500, Junior and Seniors – $5,500.

Direct Unsubsidized Loans — Students are not required to demonstrate financial need to receive a Direct Unsubsidized Loan (FAFSA is still required for this type of loan). Much like subsidized loans, Pratt determines the amount you can borrow. Interest accrues (accumulates) on an unsubsidized loan from the time it’s first paid out to Pratt. Students can pay the interest while in school and during grace periods and deferment or forbearance periods, or allow it to accrue and be capitalized (that is, added to the principal amount of your loan). If a student chooses not to pay the interest as it accrues, this will increase the total amount you have to repay because you will be charged interest on a higher principal amount. Undergraduate students are allowed to borrow an additional Annual Unsubsidized Loan of $2,000 as a Freshman, Sophomore, Junior, and Senior.

NOTE: All independent students and dependent student whose parent was DENIED (Documentation of denied PLUS Loan may be required) a Parent PLUS Loan may be eligible for additional unsubsidized loan amounts. For Freshman and Sophomores the additional unsubsidized Stafford Loan is $4,000. For Juniors & Seniors the additional unsubsidized Stafford Loan is $5,000.

Aggregated Direct Loan Limits (Subsidized and Unsubsidized):

Undergraduate Dependent Students:

$31,000 (no more than $23,000 of which can be subsidized).

Undergraduate Independent Students:

$57,500 (no more than $23,000 of which can be subsidized).

Direct PLUS Loans for Parents – Parents of dependent students may apply for a Direct PLUS Loan to help pay their child’s education expenses as long as certain eligibility requirements are met.

To be eligible for a Direct PLUS Loan for Parents:

- The parent borrower must be the student’s biological or adoptive parent. In some cases, the student’s stepparent may be eligible.

- The student must be a dependent student who is enrolled at least half-time at Pratt. Generally, a student is considered dependent if he or she is under 24 years of age, has no dependents, and is not married, a veteran, a graduate or professional degree student, or a ward of the court.

- The parent borrower must not have an adverse credit history (credits check will be done). If the parent does not pass the credit check, the parent may still receive a loan if someone (such as a relative or friend who is able to pass the credit check) agrees to endorse the loan. The endorser promises to repay the loan if the parent fails to do so. The parent may also still receive a loan if he or she can demonstrate extenuating circumstances.

- The student and parent must be U.S. citizens or eligible noncitizens, must not be in default on any federal education loans or owe an overpayment on a federal education grant.

Interest is charged from the date of the first disbursement until the loan is paid in full. The parent will pay an origination fee of the loan amount, deducted proportionately each time a loan disbursement is made. The repayment period for a Direct PLUS Loan begins when the loan is fully disbursed, and the first payment is due 60 days after the final disbursement. The parent will repay the servicer listed on the disclosure statement provided when he or she received the loan. The Direct PLUS Loan Program for parents offers three repayment plans-standard, extended, and graduated-that are designed to meet the different needs of individual borrowers. The terms differ between the repayment programs, but generally borrowers will have 10 to 25 years to repay a loan.

Information on interest rates and origination fees.

Key Changes for New Borrowers (Effective July 1, 2026):

On July 4, 2025, the One Big Beautiful Bill Act (OBBBA) was signed into law, resulting in changes to federal student aid programs. Some of these changes went into effect immediately, while others will go into effect in 2026 and beyond. Go to One Big Beautiful Bill Act Updates for the most recent updates about this law.

Parent PLUS Loans Capped: New limits of $20,000/year and $65,000 lifetime per dependent student.

Overall Lifetime Cap: A new $257,500 lifetime limit applies to all federal loans (excluding Parent PLUS).

Legacy Provisions:

Existing Borrowers: Those with loans before July 1, 2026, can continue borrowing under older rules for their current program or for three more years, whichever is shorter.

How to Apply

Direct Subsidized/Unsubsidized & PLUS Loans are generally included as part of a student’s award package (based on eligibility), which may contain other types of aid to help meet the costs of attendance at Pratt Institute.

- Complete the FAFSA online at FAFSA® Application | Federal Student Aid using the PIN as an electronic signature. To apply for a PIN or receive a duplicate copy visit Create an Account (FSA ID). Once the application has been completed, print out the application and Confirmation Page for record keeping. Be sure to use our school code: 00279800 to ensure we receive your application without delay.

- Students and Parents receiving a Direct Loan for the first time must complete a Master Promissory Note (MPN). The MPN is a legal document in which the borrower (student or parent) promise to repay their loan and any accrued interest and fees to the Department of Education. It also explains the terms and conditions of each loan type. If a student/parent previously signed an MPN to receive a FFEL (lender based) Program loan or Direct Loan 10 years ago, a new MPN will need to be signed for a Direct Subsidized/Unsubsidized & PLUS Loan to be processed.

- A MPN can be used for Direct Subsidized/Unsubsidized and PLUS Loans being received over several years of study, however a Parent PLUS Loan Authorization Form or Graduate PLUS Loan Authorization Form MUST be filled out each school year confirming the actual amount to be borrowed in the Direct Subsidized/Unsubsidized, and PLUS loans. NO LOANS WILL BE CERTIFIED AND ORIGINATED FOR DISBURSEMENT WITHOUT A PARENT PLUS LOAN AUTHORIZATION FORM OR GRADUATE PLUS LOAN AUTHORIZATION FORM ON FILE

- Undergraduate students who have not previously received a FFELP (lender based) or Direct Subsidized or Unsubsidized Loan at Pratt Institute must complete Direct Loan Entrance Counseling before they can receive the Subsidized or Unsubsidized Loan disbursement. The Direct Loan Entrance Counseling can be electronically completed via Entrance Counseling | Federal Student Aid. A Federal Student Aid PIN (FAFSA PIN) is required to complete online the Direct Loan Entrance Counseling.

The funds from each will be paid through Pratt Institute, generally in at least two installments. No installment may exceed one-half of your loan amount. If you’re a first-year undergraduate student and a first-time borrower, your loans funds will not disburse until 30 days after the first day of the semester. Pratt will use the loan funds first to pay for tuition and fees, room and board, and other billable school charges. If any loan funds remain, a refund check will be sent out to the student within 14 business days. All refund checks are mailed to the address submitted to the Registrar’s Office. If you have any questions regarding your refund checks, please feel free to contact Student Financial Services at 718.636.3599.

***In the case of a PLUS (Parent Loan) Loan, refunds checks are sent to the Parent borrower unless written authorization is given to Student Financial Services requesting that the excess funds from the PLUS loan be given to the student.

Private Loans

Private Lender Arrangement Disclosure

Pratt Institute Preferred Lender List Selection Process

Pratt Institute is committed to providing our students and their families with the best possible financial aid options. While we recognize that some students may need to utilize private education loans to help cover the cost of their education, we maintain a carefully vetted list of preferred private lenders to assist you. This disclosure outlines the rigorous process we use to evaluate and select the lenders featured on this list, in compliance with federal regulations (34 CFR § 601.10).

Maximize Federal Financial Aid First

Before applying for a private education loan, Pratt Institute strongly encourages all students and families to apply for and maximize their eligibility for Federal student aid (Title IV aid), as federal loans generally have more favorable terms and conditions than private loans.

- Maximum Federal Grant Aid: For the current academic year, the maximum Federal Pell Grant available to eligible students is $7,395

- Maximum Federal Loan Aid: The maximum annual Federal Direct Loan limits range from $5,500 to $12,500 for undergraduate students (depending on grade level and dependency status), and up to $20,500 for graduate students. Federal PLUS loans are also available up to the cost of attendance minus other financial aid.

Selection Timeline, Method, and Criteria

To ensure fairness, transparency, and that lenders are selected on the basis of the best interests of the borrowers, the Pratt Institute Financial Aid Office conducts a comprehensive Request for Proposal (RFP) process. The most recent selection process was conducted without prejudice and for the sole benefit of our students, according to the following timeline:

- November 2025: A formal Request for Proposals (RFP) was published and distributed to private student loan lenders.

- February 2026: All submitted proposals were thoroughly reviewed by the selection committee. Lenders were evaluated based on a variety of factors in the borrower’s best interest, including highly competitive interest rates, excellent borrower benefits, flexible repayment options, high-quality customer service, and technological efficiency.

- March 2026: Virtual interviews were conducted with the top-ranking lenders to further assess their services, ask clarifying questions, and ensure they meet the high standards expected for Pratt Institute students.

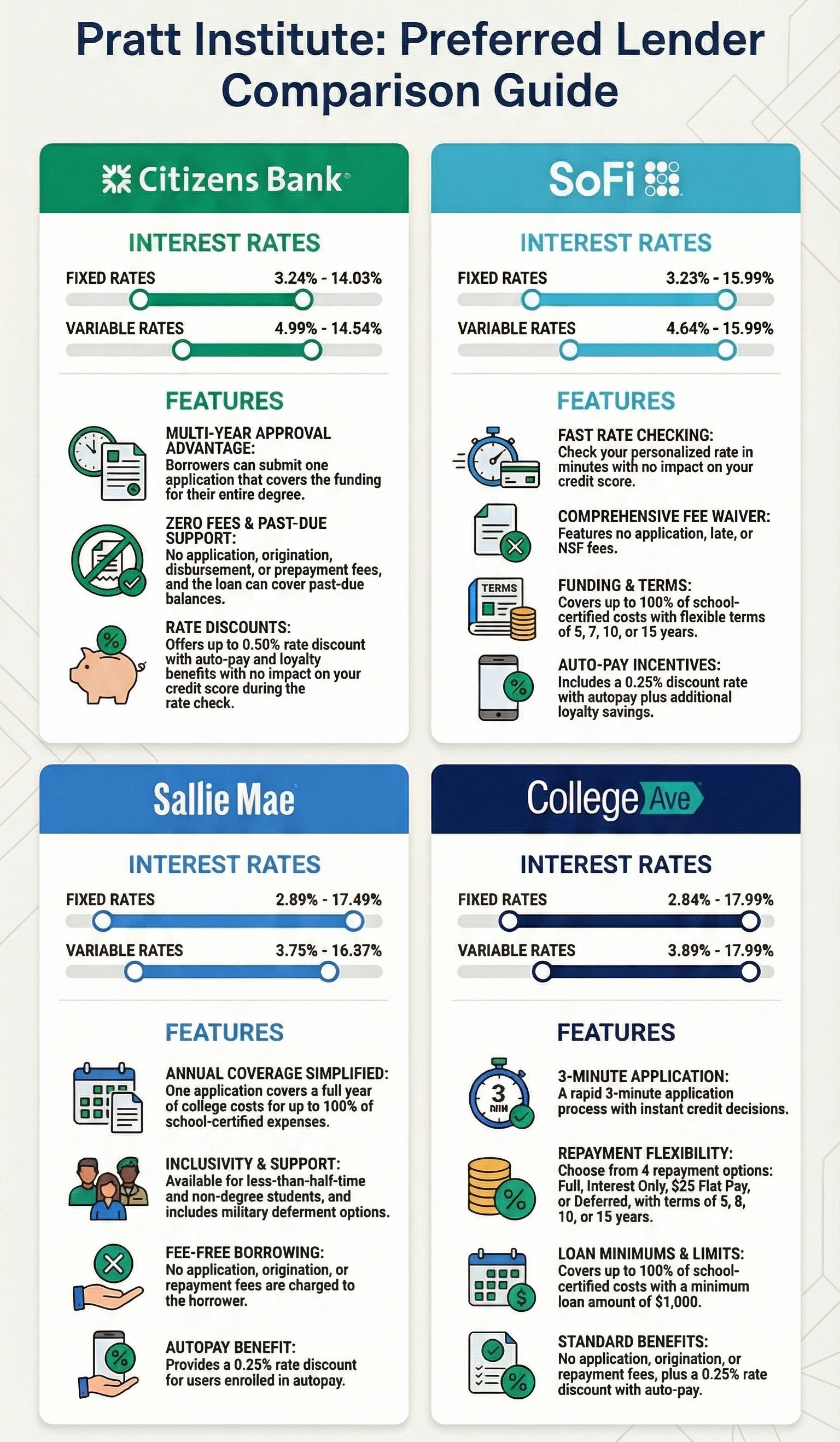

Based on this comprehensive review, Pratt Institute selected the following four lenders for our preferred lender list:

- Citizens Bank

- SoFi

- Sallie Mae

- College Ave

Please refer to the flyer for the specific loan details, interest rates, and features for these selected lenders. Additionally, detailed model disclosure forms (providing specific loan terms required by the Truth in Lending Act) for each of these lenders are available upon request or on the lender’s application portal.

{kind=link}

Lender Affiliations

In compliance with federal regulations, Pratt Institute certifies that, to the best of our knowledge, none of the lenders listed on our preferred lender list are affiliated with each other. They are separate, independent lending institutions.

Your Right to Choose

Students and families do not have to borrow from a lender on the preferred lender list. You have the right to select any private education lender of your choice.

Pratt Institute will promptly process the documents required to obtain a loan from any eligible lender you select. Your choice of lender will not affect your eligibility for other forms of financial aid, nor will Pratt Institute deny, impede, or cause unnecessary delay in the loan certification process for borrowers who choose a lender that is not included on the preferred lender list. We strongly encourage you to compare multiple lenders to find the loan terms that best fit your individual financial needs.

Code of Conduct and Conflict of Interest

Pratt Institute strictly adheres to a Financial Aid Code of Conduct, exercising a duty of care and a duty of loyalty to our students. We explicitly declare that there are no conflicts of interest between Pratt Institute, our financial aid staff, and any of the lenders on our preferred list. Furthermore:

- Pratt Institute does not participate in any revenue-sharing arrangements with any lender.

- No employee of the Financial Aid Office receives gifts, trips, or any form of compensation from lenders.

- No lender is assigned to a first-time borrower automatically.

- We do not accept offers of funds for private loans in exchange for providing concessions or promises regarding a specified number or volume of loans.

If you have any questions about this disclosure, Federal Title IV aid, or the private loan process, please contact the Office of Student Financial Services at Pratt Institute.